Rapido's claim to fame

You’re sitting in chock-a-block traffic praying your cab will make the next green light. You look out the window and a Zomato delivery boy 3 rows behind confidently steers through the tightly knit web of cars to make it to the front of the line. Annoying!! Sometimes you just want to get out of your cab and zip through the traffic on a bike.

Well, the guys who started Rapido sought to do something about this.

Ola launched in Mumbai in 2010, followed shortly by Uber in Bangalore in 2013. Both giants have been bleeding cash since their very inception. So why would Rapido willingly enter a category where even the incumbents are struggling to make money?

To answer this question, let’s go back to Rapido’s beginnings. In the early 2010s, while Ola/Uber were busy battling over the cab market in big cities, Rapido realized that most of India was being left underserved.

Market Gaps Ola/Uber Left Untapped

Lack of ride sharing service in the low ticket segment

At the time, India’s GDP per capita was ~₹7,600/month, making cabs (which typically range between ₹180-200 / ride) unaffordable for the average Indian outside a Tier 1 city. Ola/Uber were overlooking the significant commuter base in Tier 2/3 cities that demanded a cheaper service.

Huge market of 2-wheelers in India that was underutilized

Apart from being focussed on just the metro cities, Ola/Uber were catering exclusively to cab riders. They completely neglected the fact that India runs on 2-wheelers and these make up 75% of all vehicles here. When Rapido entered the ride hailing market in 2015, there were ~22 crore bikes in the country.

To top it off, around ~20% of this pool of bike owners was either unemployed, part-timing, or a student. That translated to a pool of 4.4 crore+ potential bike driver partners.

The market opportunity was / is big

Despite Ola/Uber’s negligences, the market was growing quickly at 40-50% annually.

Further, to put into context how much room for growth there is - Rapido today does 3.5 million rides/day (across bikes, autos, cabs), while Chinese (comparable population) DiDi does 30 million!

Lastly, almost 2 million autos and 2.5 million cabs run everyday in the country but online aggregation accounts for less than 10% of these, in both categories. There is ample room for expansion.

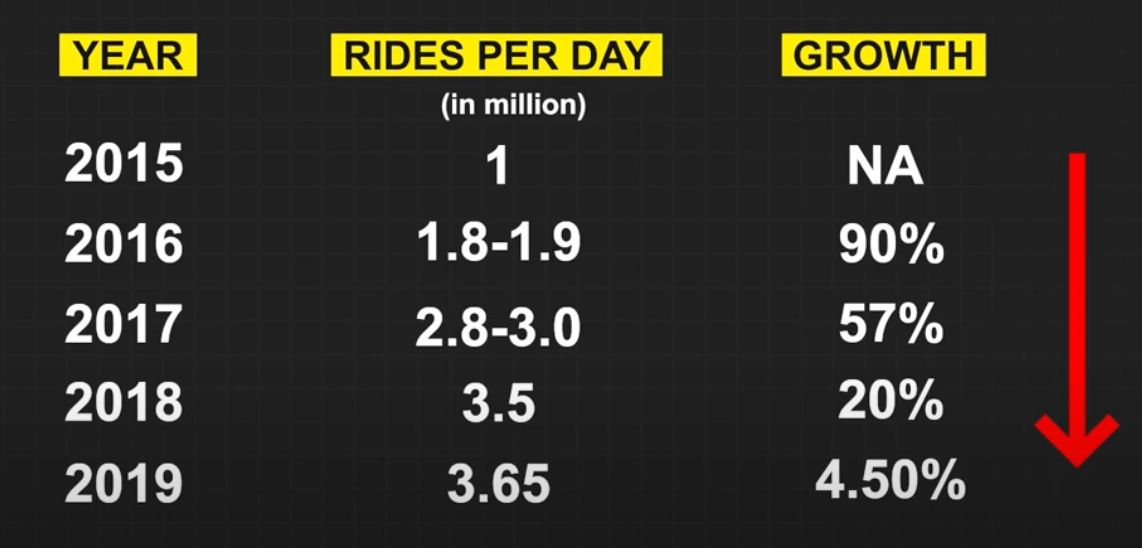

Like you can see below, Ola/Uber’s growth slowed down and rides per day peaked in 2019 which was evidence that demand for a cheaper service existed.

Rapido’s Strategic Entry Points

Category creation

Keeping all the above in mind, Rapido decided to make the genius move of pioneering bike taxis - offering a transport option to riders for just ₹60-65 a ride. They focussed primarily on expanding in Tier 2/3 cities, where customers were even more price sensitive and public transport was less extensive, instead of fighting with incumbents for the relatively saturated Tier 1 market. And bikes weren’t just cheaper, riders liked them because they were quicker too.

Supply innovation

Unlike Ola/Uber, which had to really re-invent the wheel to attract drivers to sign up, Rapido tapped into the massive supply of existing bike owners. To further their cause, it helped that the rear seats of 80% of bikes on roads were anyways vacant. That encouraged pretty much anyone with a bike and some free time to sign up as a driver (fyi - Rapido calls them Captains).

Low-risk, part-time model

In the Ola/Uber model, drivers had to take loans to buy cars and then became fully dependent on the service for their income. Rapido, on the other hand, positioned itself as a flexible, side-income opportunity with minimal financial risk for anyone looking to make an extra buck.

A More Sustainable Business Model

Driver-friendly Economics

Rapido bike drivers collect the payment from customers directly and pay just a 15% commission to Rapido later, which eases their liquidity burden. Ola/Uber on the other hand, collect payments from the customer, take as high as a 30/40% commission and disburse payments to drivers at the end of the week.

Even in the auto and cab segments, Rapido accurately detected the drivers’ pain points and clinically addressed these. For autos, they adopted a flat daily fee (of just ₹9-29/day) and in cabs, a zero-commission model with a fixed monthly fee of ₹500 (only if earnings crossed ₹10,000). This pocket-friendly model encouraged drivers to sign up on the platform in volumes.

Evidence of this is that 15% of the drivers who have signed up for Rapido cabs are new to the profession. This shows that Rapido’s model is appealing to people who were previously hesitant to join the industry. In Hyderabad (which was Rapido’s pilot market for cabs) they were able to quickly capture 23-25% of the cab market.

Lower cash burn

Ola/Uber had to create a market on both sides (riders and drivers) pretty much from scratch via insane discounts for customers and ultra low commissions for drivers. They did this in the initial phases by burning cash. The customers were thrilled to be getting discounted rides and the drivers were making a plush 50-60k a month driving a cab. In this phase, the drivers fully committed to these services, often taking up a loan to buy the new vehicles. But with time, these incentives withered while drivers’ liabilities (loans, maintenance costs etc.) stayed, thus causing drivers’ take homes to plummet and their dissatisfaction to skyrocket.

Rapido didn’t have to engage in this cash burn phase, because there were structural incentives for both the drivers (signing up was a secondary source of income on anyways idle 2-wheelers) & customers (a cheaper transport service to available alternatives) to sign up / use the service. Plus, two wheelers have low maintenance costs and very high mileage. For the part-timers, students, and unemployed, the ₹200-500 extra cash per day was a blessing, especially given such a low barrier to entry.

For this reason, Rapido (unlike its competitors) was able to achieve PAT profitability in 2024! Further, it had built its cost structures to survive on razor thin margins from bike taxis, so any margins from autos/cabs, when they expanded to these segments, became additional.

Flexibility & agility

Rapido operates on the mantra of bringing a fundamental change to their driver partners’ lives. And this has helped tremendously with their profitability. During the lockdown, they proved to be more agile than competitors, partnering with food delivery/QComm to leverage their idle fleets + state governments to deliver Covid relief. This extended even beyond the pandemic with Rapido forging a strategic partnership with Swiggy, to utilize its extensive fleet of bike and auto drivers during off-peak hours to handle food delivery services.

Regulatory loopholes

One of most critical hurdles of the bike taxi market is regulation. In fact, at the outset, regulators didn’t permit bike taxis in several states. Rapido initially leveraged grey areas by positioning itself as a bike-pooling service rather than a commercial taxi operator, allowing it to bypass stringent transport regulations. Unlike Ola and Uber, Rapido kept a low profile - using no branded vehicles or uniforms - to avoid early enforcement actions. Over time, this approach gave Rapido a first-mover advantage in the bike taxi space while formal regulatory clarity was still evolving.

Even now, Rapido claims that it is not a cab aggregator but a SaaS platform. It provides the tools to drivers to help them manage rides, payments, and pricing, while also conveniently avoiding certain scrutiny that apply to typical taxi operators.

In summary, Rapido’s entry into the cab market is a logical extension of its core strategy: building low-cost, driver-friendly mobility solutions for under-served markets. The cab segment, like bikes and autos, suffers from high commissions and driver dissatisfaction on incumbent platforms. Rapido introduced a flat-fee model, offering drivers predictable costs and better margins, thus quickly gaining traction. In Hyderabad (where Rapido piloted its cab service), it quickly captured a good chunk of market, encouraging expansion to this category nationwide. The fact that 15% of cab drivers on Rapido are new to the profession, indicates that they're growing the supply pool, not just competing for it. India’s cab and auto markets remain under-penetrated online (less than 10% digitized), especially in Tier 2/3 cities. Rapido’s low-friction, capital-efficient model is well-positioned to onboard this untapped supply. Lastly, recent funding of $200 million from WestBridge and Swiggy gives Rapido the capital to scale and experiment aggressively in this category.